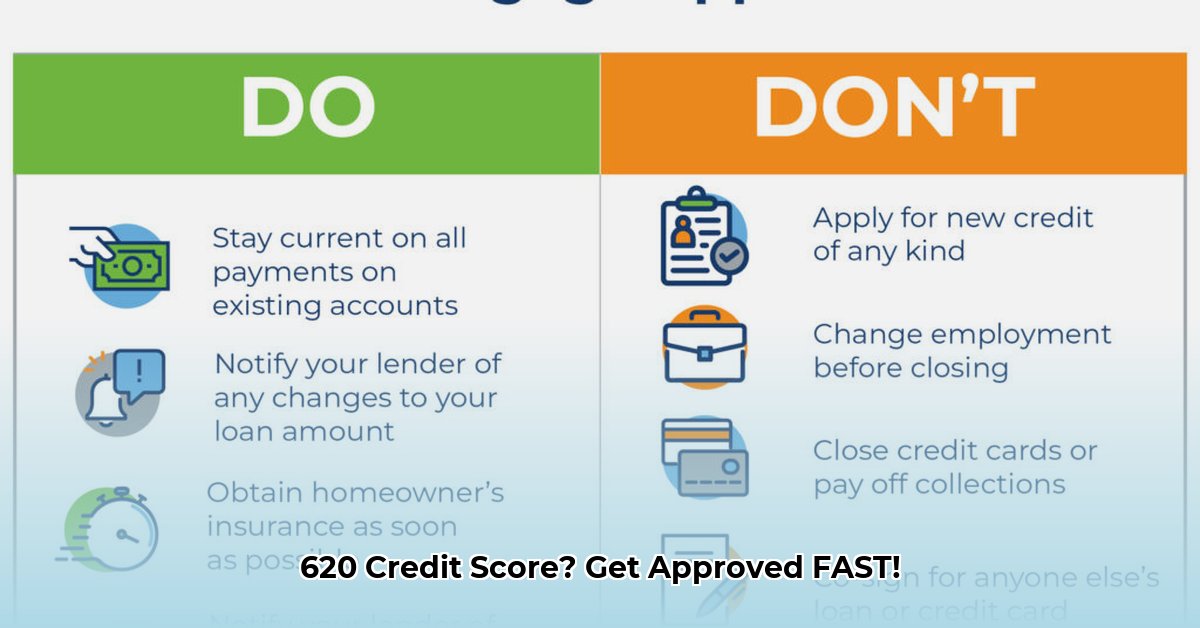

MortgagePossible is disrupting the mortgage lending landscape with its promise of rapid loan approvals, even for borrowers with credit scores as low as 620. This accelerated process, however, prompts crucial questions regarding risk assessment, regulatory compliance, and the long-term viability of its model. While expanding access to homeownership is laudable, the inherent risks necessitate a cautious approach.

Expanding Access: A Double-Edged Sword

MortgagePossible aims to serve underserved borrowers often overlooked by traditional lenders. Credit scores below 620 typically preclude mortgage approval, but MortgagePossible seeks to bridge this gap, opening homeownership to a broader population segment. This expansion, however, introduces heightened risk, requiring a careful balance between inclusivity and responsible lending. But how does this increased access manifest in actual risk for the company and the borrower?

Speed and Technology: Efficiency versus Oversight

MortgagePossible's 60-second online application process relies on sophisticated technology to automate underwriting. This rapid turnaround appeals to many but raises concerns. Can automated systems accurately assess the risk associated with higher-risk borrowers? Is sufficient human oversight implemented to address potential errors or unusual circumstances? The speed of the process, while advantageous, could potentially sacrifice due diligence, creating considerable uncertainty.

Risk Assessment: A High-Stakes Calculation

MortgagePossible's model involves accepting higher-risk loans, characterized by lower credit scores and high Loan-to-Value (LTV) ratios—sometimes reaching 97%. The frequent waiver of traditional appraisals, relying instead on automated valuations, further amplifies this risk. While this may accelerate the process, it raises questions around accuracy and the potential for increased defaults. Their claim of a "100% trusted warranty" needs further detailed clarification regarding its scope and limitations.

| Risk Factor | Severity Level | Potential Impact | Mitigation Strategies (Claimed) |

|---|---|---|---|

| High LTV Ratios | Very High | Increased default potential if home values decline. | Diversified loan portfolio; sophisticated risk-scoring models |

| Appraisal Waivers | Very High | Potential for inaccurate property valuation. | Alternative valuation methods; stringent underwriting |

| Lower Credit Score Borrowers | High | Higher likelihood of borrower financial distress. | Alternative data analysis; strengthened underwriting criteria |

| Automated Underwriting System | Medium | Possible errors or biases in automated risk assessment. | Human oversight; regular system audits; ongoing algorithm refinement |

Regulatory Compliance: Navigating a Complex Landscape

MortgagePossible's lending practices operate near the edges of regulatory scrutiny. High LTV ratios, appraisal waivers, and lending to borrowers with lower credit scores invite intense regulatory oversight. Adherence to fair lending standards and transparent practices is essential. Non-compliance could result in substantial legal challenges and penalties. The evolving regulatory environment presents a significant challenge to the company's long-term sustainability. The question becomes, can they consistently adapt to the ever-changing landscape of lending regulations?

Conclusion: A Balanced Perspective

MortgagePossible's disruption of the mortgage market offers the potential for greater accessibility to homeownership; however, its high-risk lending model poses significant challenges. While the speed and convenience are undeniably appealing, potential borrowers should exercise extreme caution. The current model's long-term viability depends on the successful mitigation of these risks and sustained regulatory compliance. Thorough independent research and consultation with a financial advisor is strongly recommended before engaging with their services. A short-term outlook presents a high-risk, high-reward scenario, while a long-term prognosis hinges on their ability to navigate regulatory pressures and consistently manage their risk exposure. Careful due diligence is paramount.